For many franchisees, financing is the final, and often most stressful, step between signing an agreement and opening the doors. While Small Business Association (SBA) loans have long been the go‑to option for first‑time operators, recent policy changes have shifted how, when, and even if those funds are released.

Understanding the difference between SBA-backed franchise loans and traditional bank loans, and how the SBA landscape has changed, can save franchisees months of delays, unexpected cash gaps, and missed opportunities. Here’s what franchisees need to know about franchise financing:

What’s Changed at the SBA (That Actually Matters to Franchisees)

The SBA Franchise Directory is back, and it’s mandatory. As of June 1, 2025, a franchise brand must be listed in the SBA Franchise Directory for a franchisee to qualify for SBA financing. Brands that are not listed, or that fail to submit updated certifications, block SBA funding entirely until reinstated. Ensure that your franchisor is listed and is compliant. There is no workaround. Franchisees are fully dependent on the brand’s compliance status.

Higher Underwriting Standards for New Units

The SBA’s official Standard Operating Procedure, known as SOP 50 10 8, governs how SBA-backed loans are underwritten, approved, documented and funded. Lenders are now required to apply stricter underwriting criteria:

- 10% cash injection for all startups and ownership transfers

- Higher SBSS (Small Business Scoring Service) credit thresholds

- 165+ for small loans

- Many banks now require 680–700+ personal credit

- Working capital must be itemized and justified

- Collateral requirements reinstated for loans over $50,000

- “Credit elsewhere” test is back – if a borrower can reasonably self‑fund, SBA financing may be denied.

For franchisees, this means the bar has been raised. Marginal borrowers who may have qualified in the past will struggle, while strong candidates can still move forward, but only with cleaner files and more thorough documentation.

More Lender Scrutiny, Less Discretion

Lenders now carry greater compliance responsibility and face higher audit risk. As a result, lenders are:

- Moving slower

- Asking for more documentation

- Re‑underwriting deals later in the process

For franchisees, this means fewer quick approvals and more deals approved with conditions that must be cleared before funds are released. In today’s SBA environment, approval is no longer the end of the process; it’s just the halfway mark.

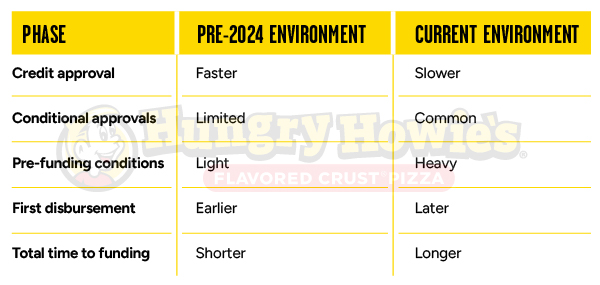

How These Changes Affect the Timing of Funding

Under the new SBA rules, loan approval happens earlier, but funding happens later. Why?

Before funds are released, lenders must now re‑verify:

- Environmental (site assessment) reports

- Franchise Directory status

- Full equity injection

- Lease execution, entity formation, and permits

Funds are released much closer to opening, not at approval. This is a major policy shift that catches many franchisees off guard.

The New Funding Timeline Reality

While timing varies by lender, the overall trend is clear. Lenders are emphasizing risk mitigation and staged disbursements, not speed.

Construction and Build‑Out Draws Are Now Standard

Construction and build‑out franchise funding is now typically released in stages, not as a lump sum. Initial draws may cover items like franchise fees or equipment deposits, while final funds are often held until the space is complete, and personal funds have been fully deployed. As a result, franchisees should plan for more upfront bridge capital and longer timelines if they expect full funding at approval.

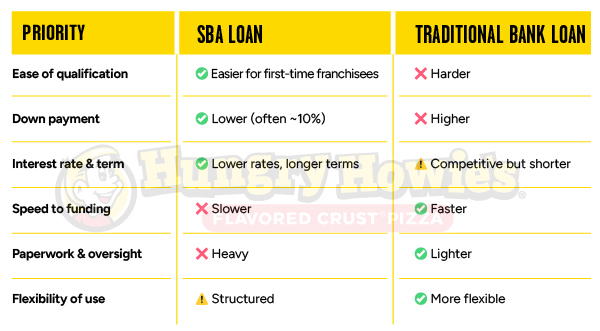

The Core Trade‑Off: SBA Franchise Loans vs. Traditional Bank Loans

SBA franchise financing is designed to expand access and lower upfront costs, whereas traditional loans are better suited for borrowers who value speed and simplicity.

When a Traditional Loan Can Make More Sense

A conventional bank loan is often the better option when most of the following are true:

Strong borrower profile

- Excellent personal credit (often 700+)

- Significant liquidity beyond minimum equity

- Strong net worth and collateral

Proven operating experience – this is often the biggest hurdle.

- Multi‑unit operator

- Franchise resale or acquisition

- Prior success in QSR or retail operations

- A well‑thought‑out business plan

Time‑sensitive deal

- Real estate deadlines

- Construction already underway

- Need funds quickly to secure a site or contractor

Established brand

- Long operating history

- Strong unit‑level financials banks already understand

In these cases, traditional banks can move faster, and may even price competitively, without SBA red tape.

Ultimately, the right franchise financing strategy isn’t one‑size‑fits‑all. Successful franchisees treat financing as a strategic decision, not just a source of capital—balancing access and affordability against speed and flexibility based on their goals and timeline. Because these choices can have long‑term legal and financial implications, it’s best to consult with your attorney or CPA when evaluating financing options and structuring your funding strategy.

With the right guidance, franchise financing becomes a tool for long-term growth – not a constraint. Understanding your options now can help you move forward with confidence and clarity. Ready to investigate franchising opportunities with Hungry Howie’s? Learn more.